Award-winning PDF software

433-b oic Form: What You Should Know

YouTube · Tax Resolution Professionals · Sep 12, 2025 · 01:02 UTC 733-B — Collectible Items For Purposes of Federal Income Taxes For purposes of the federal income tax, the Internal Revenue Service (IRS) Taxpayer Relief Act of 2025 (“Act”) and Treasury Regulations establish the general definition of a collectible (in § 1041(e)) and the tax treatment of certain collectibles. Collectibles include (a) tangible personal property; and (b) property which satisfies the test for valuation set forth in (e) of this section. The Regulations provide the following guidelines for computing capitalization of tangible personal property used in the ordinary course of a trade or business: (i) property used in the ordinary course of a trade or business in at least two (2) days of the year of its use is deemed to have been used in the trading, business or farm activity in at least two (2) days of the year; (ii) property used in the ordinary course of the trade or business in at least one year is deemed to have been used for the trading, business or farming activity in all the years of its use, and (iii) property used in the trade or business in any year is deemed to have been used as inventory. Income from the sale or distribution of tangible personal property used in the ordinary course of a trade or business is included within the capital gains of the taxpayer, provided that the property is used in the carrying on of a trade or business within the 12-month period leading up to the distribution. If property used in the ordinary course of a trade or business can be excluded from taxable income by reason of a transfer to a qualified beneficiary in a qualified transferor-provision vehicle that is not treated by the Secretary as a transfer of property by reason of section 514(a)(1)(D), the use of such property in the course of such trade or business during such 12-month period shall be disregarded as a trade or business. A taxpayer's business use of inventory that constitutes inventory for purposes of determining the amount of any deduction provided by section 168 is not considered to be used in the business of a real estate broker.

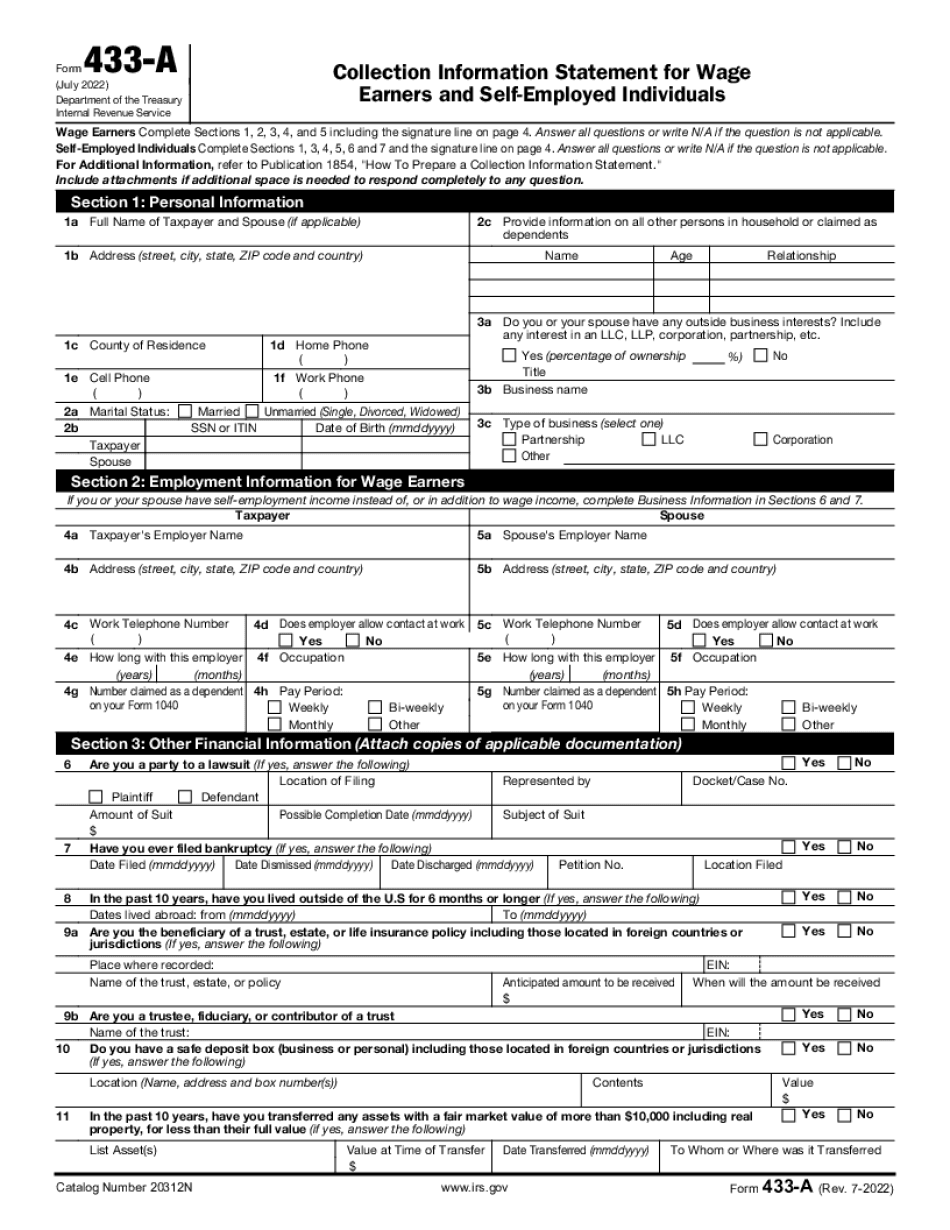

Online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 433-a, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 433-a online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 433-a by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 433-a from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.